Yes. Solar remains one of the most effective ways for New Yorkers to combat some of the highest and fastest-rising electricity rates in the country.

While the federal tax landscape for solar purchases changed on January 1, 2026, New York homeowners have multiple paths—including direct ownership and Third-Party Owned (TPO) models—to lock in long-term savings. Whether your goal is immediate monthly savings or the highest possible long-term ROI, solar is “worth it” in 2026 as a hedge against a volatile grid.

The 2026 New York Energy Reality: Rising Costs and Shifting Incentives

New Yorkers are currently facing a “perfect storm” of energy costs. With major investments in grid modernization, utility companies are passing those expenses to consumers through increased electricity rates.

-

High Power Prices: In 2026, average residential rates have climbed to between 23 and 27 cents per kilowatt-hour (kWh)—well above the national average—and rates are rising in 2026 for at least three utilities service New York (see below).

-

The Federal Tax Shift: The homeowner-claimed tax credit for buying solar expired at the start of this year. However, New York still offers a 25% state tax credit worth up to $5,000. Plus, Third-Party Owned (TPO) solar options can still access a business-claimed federal tax credit through the end of 2027.

-

The “Winter Proof” Strategy: New York’s net metering policies allow you to use the grid like a giant battery. You “bank” excess power during the long summer days to offset your heating and lighting costs during the dark winter months. Favorable net metering policies are becoming rare, and New Yorkers would be wise to lock in the current structure before it’s gone.

Notable New York Rate Hikes in 2026

| Utility | Rate Increases |

| Consolidated Edison (ConEd) | Annual rate hikes approved through 2028 |

| New York State Electric & Gas (NYSEG) | $33 increase to average monthly bill proposed for April 2026 |

| Rochester Gas & Electric | $33 increase to average monthly bill proposed for April 2026 |

Choosing Your Path: Three Ways to Save in 2026

There are three basic options to reduce your electricity costs with solar in New York. The “right” strategy depends on your savings goals, cash position, and preferences.

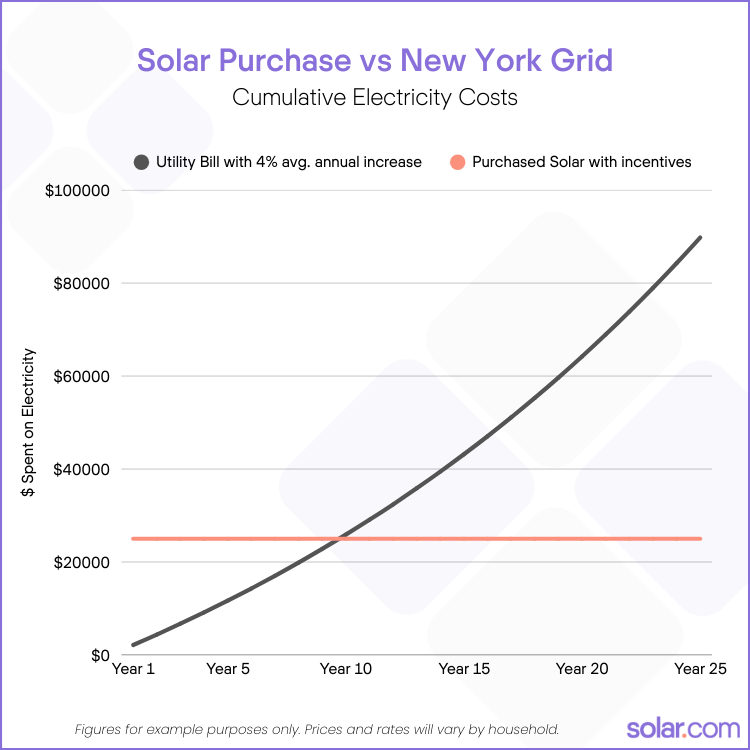

Direct Ownership (Cash or Loan)

Purchasing solar with cash or a loan offers long-term cost savings, full control over equipment selection, and added value to your home. It also means being responsible for monitoring, maintaining, and insuring your system throughout its lifetime.

-

Why it’s worth it: While the federal solar tax credit has expired for residential solar purchases, the New York State Solar Tax Credit is alive and well. New York allows owners to claim 25% of the system cost (up to $5,000) against their state income taxes to reduce the net cost of going solar.

-

Best for: Homeowners who want to invest in long-term savings, control equipment and usage, and increase their property value.

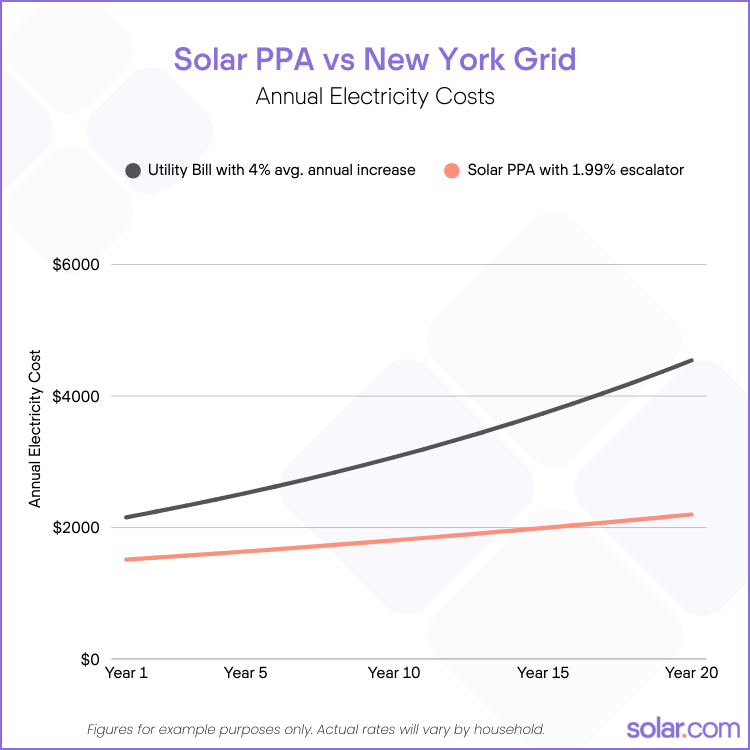

Standard Lease or Power Purchase Agreement (PPA)

Standard leases and PPAs are like switching utility providers (i.e., a third-party solar company) to replace your electricity bill with a lower, more predictable cost for solar. The lease or PPA provider owns the system, provides monitoring and maintenance, and claims federal incentives to reduce your monthly payments.

-

Why it’s worth it: Leases and PPAs still qualify for a federal tax credit through the end of 2027. The provider claims the commercial tax credit (Section 48E) and passes that value to you via a lower monthly rate.

-

Best for: Homeowners who want $0-down solar and immediate monthly savings without taking on a loan or maintenance responsibilities.

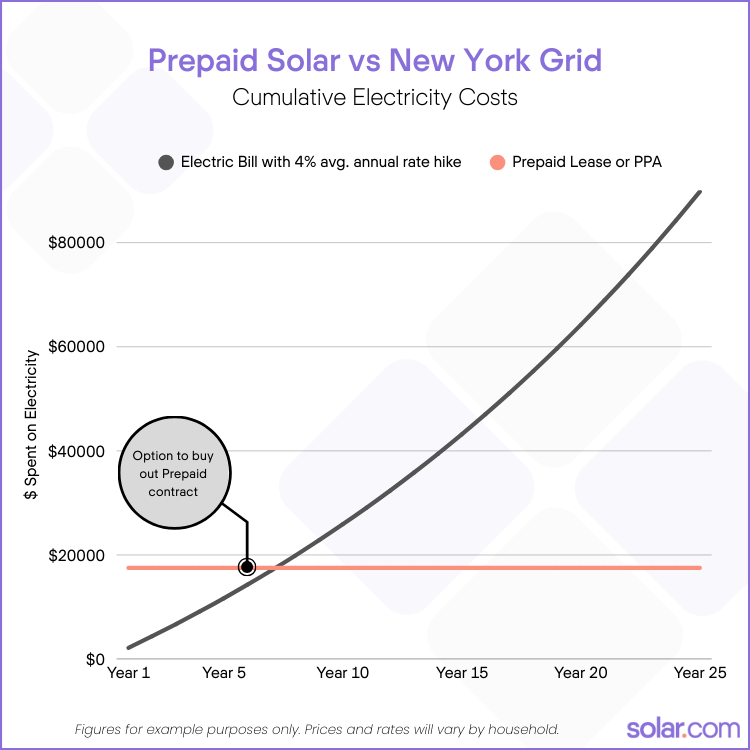

Prepaid Solar

Prepaid Solar is an emerging financing option that allows you to pay for solar energy upfront, at around 70% of the cost to purchase a solar system. The Prepaid provider initially owns the system, provides monitoring and maintenance, and claims the 48E federal tax credit. In Year 6, there is usually an option for you to “buyout” the contract and take ownership of the system (typically for little to no cost, since the balance is paid upfront).

-

Why it’s worth it: This combines the “no monthly bill” benefit of ownership with the security of a third-party monitoring and maintaining the system in its early years. Because it is technically a Third-Party Owned system, the solar company can claim a federal tax credit to lower your prepayment amount.

-

Best for: Cash buyers who want the highest possible return on investment and the peace of mind of a third-party being responsible for maintenance and repairs while the system is new and most likely to experience issues.

Which path best suits your savings goals? Team up with a solar.com Energy Advisor to review custom proposals and see your savings potential.

The “New York Bonus” Incentives

Regardless of which path you choose, New York offers several “stackable” benefits that make solar worth it in 2026:

-

NYS Solar Tax Credit: A direct reduction of your state tax liability by up to $5,000. In many cases, you can claim this credit for Third-Party Owned solar, but situations may vary based on your specific agreement and tax situation.*

-

15-Year Property Tax Exemption: Purchasing solar panels increases your home’s value, but New York law prevents your property taxes from increasing as a result for 15 years.

-

State Sales Tax Exemption: Solar equipment and installation are exempt from New York state sales tax, saving you thousands in a direct purchase.

*This article does not constitute tax advice. Consult a licensed tax professional regarding your personal tax credit eligibility.

The Verdict: Is Solar Worth It in New York?

In 2026, New York solar is about hedging against rapid and volatile utility rate increases. Whether you choose to own your system to build home equity or opt for a TPO plan to lower your monthly overhead, solar is a “worth it” investment because it replaces an unpredictable, rising utility bill with a stable, lower-cost energy source.

Schedule a strategy session with an expert Energy Advisor to find your best path to solar savings.

Frequently Asked Questions for New Yorkers

Did I miss the federal tax credit?

If you choose a Third-Party Owned (TPO) plan, no. A business-claimed tax credit is still active through the end of 2027 and can be used to lower your solar costs. If you buy the system outright, the federal 25D credit is no longer available, but you can still claim the New York State credit, worth 25% of the system cost up to $5,000.

Is solar worth it if I have a small or shaded roof?

It depends. With New York’s high utility rates, even a smaller system can provide a significant return. Our platform uses satellite imaging and a solar irradiance scoring system to identify if a roof is suitable for solar. If it’s not, we’ll be the first to tell you!

What happens if it snows on my panels?

Snow usually slides off solar panels quickly (and cleans them) because they are smooth and installed at an angle. Even if they are covered for a day or two, New York solar systems are sized based on annual production, so a few snowy days won’t ruin your yearly savings.