While going solar carries the reputation of having a high upfront cost, more than half of solar owners choose to finance with solar loans. And many of those solar loans come with zero down payment.

In fact, some homeowners with the means to pay cash choose to finance with a solar loan instead. That's because a solar loan can provide immediate energy cost savings and leave more cash in your pocket.

In this article, we'll explore the basics of solar loans, including:

Let's dive in with a look at how combo and reamortization solar loans work.

Rather speak to an Energy Advisor about solar loans? Get started here.

Solar loans 101: Reamortization and Combo loans

Solar loans are a little different than a home mortgage or car loan because they are designed to accommodate the

30% federal solar tax credit* by essentially delaying the down payment until the credit comes through.

In fact, there are two types of zero-down solar loans designed with the tax credit in mind: Reamortization loans (aka "re-ams") and combo loans.

*Update: With the "One Big Beautiful Bill" now law, the 30% solar tax credit claimed by homeowners ends on December 31, 2025. Systems must be installed by the end of 2025 to qualify for this credit before it's gone.

Reamortization solar loans

Although it's a bit of a mouthful, reamortization solar loans are used by around 60% of solar borrowers and are tailored for homeowners -- often retirees -- who aren't sure if they have sufficient income to

claim the 30% solar tax credit all in one year.

These loans are still being offered to homeowners who install their systems in 2025 and are eligible to claim the tax credit before it's gone.

Hold up, what does reamortization mean? Reamortization is when you make a lump sum payment toward the principal of your loan in order to lower the monthly payments moving forward.

In a re-am solar loan, borrowers are allowed a free, one-time reamortization to accomodate the solar tax credit -- although the money for the lump payment can come from anywhere and at anytime. Elsewhere in the lending world, there are typically servicing fees for reamortizing a loan.

The principal balance of a reamortization loan is based on the

contract price of the system before the tax credit is applied. Here's how that would look for a 20 year re-am loan with a 4.5% interest rate for a $20,000 system.

| Age of loan |

Borrower A |

Borrower B |

| Months 1-24 |

$127 |

$127 |

| Reamortization lump payment |

$6,000 |

$9,000 |

| Months 25-240 |

$86 |

$65 |

| Cumulative cost over 20 years |

$21,624 |

$17,088 |

There are a few advantages of reamortization loans:

- There is no timeline for making your lump sum payment

- You can reamortize with a lump sum payment for more than the value of the tax credit (like Borrower B) to further reduce payments

- You can forego the lump payment altogether to free up cash for something else

At the end of the day, the ideal solar loan type largely depends on your preferences and whether you can claim the full solar tax credit in one year or not.

Related reading: How To Wrap The Cost of Solar Panels Into Your Mortgage

Solar combo loans

*Update: With the tax credit ending at the end of 2025, most lenders are eliminating their combo loan offerings.

Solar combo loans are the preferred choice for borrowers who are confident they have the tax liability (based on their income) to claim the full solar tax credit in one year.

Consult a licensed tax professional with questions regarding your tax liability.

Combo loans are aptly named because they are, in fact, a combination of two loans:

- First, there is a primary loan for the net cost of the system

- Second, there is a bridge loan for the value of the tax credit

So, if you are buying a $20,000 solar system, the primary loan balance would be $14,000 and the bridge loan balance would be $6,000.

The borrower typically has 12-18 months to claim the tax credit and use it pay off the bridge loan -- although the bridge loan can be paid off with money from anywhere. If the bridge loan isn't paid off in time, the balance is rolled into the primary loan, which raises the monthly payments.

Here's how that looks for a 20-year combo loan with a 4.5% interest rate for a $20,000 system.

|

Borrower A |

Borrower B |

| Down payment |

$0 |

$0 |

| Monthly payment for first 18 months |

$89 |

$89 |

| Month 18 |

Bridge loan paid off |

Bridge loan not paid off |

| Monthly payment for months 19-240 |

$89 |

$128 |

| Cumulative cost over 20 years |

$21,360 |

$30,018 |

The figures and interest rates in the table above are for example purpose only and do not constitute an offer to lend.

The advantage of a combo loan is that your payments are initially based on the

net cost of the system, in this case $14,000 instead of $20,000.

However, if you don't pay off the bridge loan in time, the loan balance goes up, leading to higher principal and interest payments.

Solar loan terms, interest rates, and monthly payments

If nothing else, solar loans are very flexible. You can pay anywhere from 0% to 100% for a down payment, and you can also set the term -- or length -- of your loan for anywhere between 5 and 25 years (although 8-20 years is more typical).

Solar loan borrowers tend to favor 12-year and 20-year terms, with a slight edge toward 12 years.

As a rule of thumb:

- A shorter loan term means higher monthly payments, but less money paid toward interest

- A longer loan term means lower monthly payments, but more money paid toward interest

The table below illustrates this dynamic based on a combo loan for a $20,000 solar system.

| Term |

8-year |

12-year |

15-year |

20-year |

| Interest rate |

6% |

5% |

8% |

9% |

| Initial monthly payment |

$183 |

$129 |

$133 |

$125 |

| Lifetime interest paid |

$3,662 |

$4,645 |

$10,082 |

$16,230 |

The interest rates shown above are for example purposes only. This is not an offer to lend or a reflection of current interest rates.

Yes, that's a lot of numbers and loan jargon. But here's the cool thing: When you are designing a solar loan, you are essentially setting your own electricity price for the next 25 years.

Let's say a 5.7 kW solar system costs $20,000 ($14,000 after the tax credit) and produces 208,000 kWh of electricity over its 25-year warrantied life.

- If you take out a 12-year combo loan, you pay $18,645 for the system for a levelized cost of 8.9 cents per kWh.

- If you take out a 20-year combo loan, you pay $30,230 for the system for a levelized cost of 14.5 cents per kWh.

For reference, the

national average price for grid electricity is 19 cents per kWh in the summer of 2025, and

above 30 cents per kWh in California, Connecticut, Massachusetts, and Hawaii.

Not only are you controlling your electricity rate (something you could never do without going solar), you're also choosing

when you will see your solar savings.

Long-term versus short-term savings

The key question for picking the right solar loan for you is, "When do I want my savings to kick in?"

As a rule of thumb:

- A shorter loan term means a longer payback period, but greater lifetime savings

- A longer loan term means a shorter payback period, but lesser lifetime savings

So, say you live in New York and your electricity rate is 20 cents per kWh and rising on average of 3% per year. You could go for instant bill savings with a longer-term loan, or maximum lifetime savings with shorter-term loan.

|

8-year |

12-year |

15-year |

20-year |

| Payback period |

10 years |

None |

None |

None |

| Savings year 1 |

-$527 |

$120 |

$72 |

$168 |

| Savings year 5 |

-$2,122 |

$1,117 |

$877 |

$1,357 |

| Savings year 10 |

$1,558 |

$3,646 |

$3,166 |

$4,126 |

| Lifetime savings |

$43,260 |

$42,252 |

$36,888 |

$30,828 |

As you can see above, the 20-year loan offers the greatest bill savings up front, but the 8-year loan offers the greatest savings over the 25-year warrantied life of a solar system.

A 12-year term offers a good balance of both, and is the most common loan term chosen by solar.com customers.

Solar loan interest rates

If you choose to finance with a solar loan, you're going to end up paying interest. That's just part of the deal.

Much like mortgage rates, solar loan interest rates rise and fall based on macroeconomic forces. They plummeted during the pandemic and have been rising since mid-2022.

While there is little anyone can do about macroeconomics, there are two things you can do to lock in a lower interest rate.

- Increase your credit score. A 650 FICO score is typically the minimum credit score required to qualify for a solar loan. Having a score between 680 and 719 can help you qualify for a better rate, and have a score above 720 can help you qualify for the best rate.

- Move quickly. Interest rates are expected to continue rising throughout 2023. That means the sooner you qualify for a loan and lock in an interest rate, the lower it will be.

Keep in mind, although the interest rate on your solar loan does matter, it's not always wise to wait around for rates to drop. That would be like stepping over a $20 bill to pick up a $1 bill.

Going solar is a long-game, and the sooner you go solar, the longer you can accumulate savings.

Solar loan qualifications

Just like a mortgage or car loan, solar lenders have qualifications that borrowers need to meet in order to be approved for a loan.

Solar loan qualifications may vary by lender, but in general they include:

- FICO credit score of 650 or above

- Debt-to-income (DTI) ratio below 50%

- The primary borrower must have their name on the title of the home getting solar panels

In some cases, adding a co-borrower with a strong credit score and DTI can help you qualify for a solar loan.

It's also worth noting that there are different kinds of credit scores, and the one you got for free online may not be the score solar lenders use to approve your loan application.

To avoid surprises, come into the process knowing your FICO score.

Is Solar Financing Good Debt or Bad Debt?

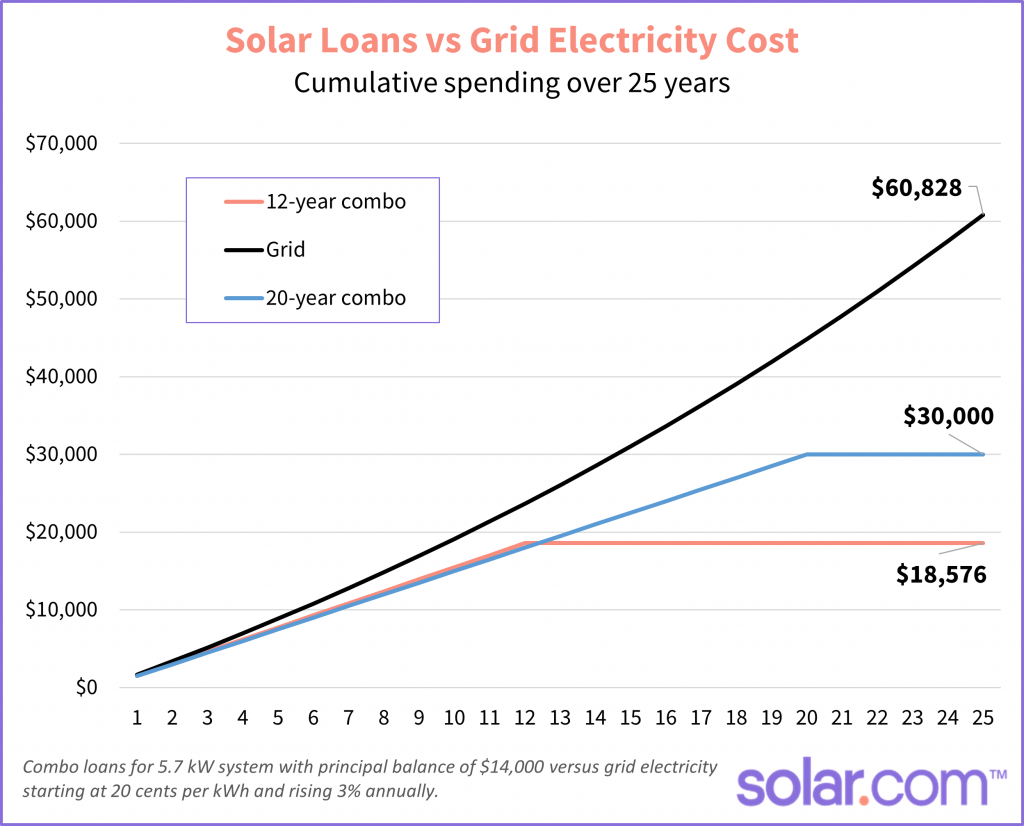

Some financial advisors encourage consumers to avoid debt, or to at least evaluate whether a debt is good debt or bad debt. In the case of solar, there is compelling evidence that solar debt is a unique case of good debt.

How Stuff Works defines good debt as: “An investment that will grow in value or generate long-term income.”

Examples include a college education which will significantly increase your earning power, or a mortgage for a home which will lock in your shelter cost and is expected to increase in value over time.

By that same definition,

solar is a very good investment because it shields you from rising electricity prices, as shown in the graph below.

Yes, it costs money to purchase the system and pay off interest on a loan. However, that investment more than pays for itself in energy cost savings over the 25-year warrantied life of a the solar panels.

How to find a solar lender

There are a few ways to find a solar lender.

- Find one yourself

- Use a lender recommended by your solar installer

- Team up with a solar.com Energy Advisor to compare vetted lenders their rates

While you can certainly use your regular bank or credit union to finance a loan for your solar panels, they may not offer the combo and reamortization solar loans described above.

Your solar installer will likely recommend a lender that they work with often, but they won't help you shop around for the best rate.

If you go solar through solar.com, your dedicated Energy Advisor will walk you through loan options

and help you shop for loans. We understand that the loan process can feel complex and overwhelming, but it's something they navigate every day, and they're happy to guide you through it.

Team up with an Energy Advisor to navigate the solar process.

PACE Solar Loans

There is also a government program called

PACE (Property Assessed Clean Energy).

PACE makes solar more accessible to lower-income or credit-challenged households by allowing homeowners to use their home as collateral to finance their solar system.

Note, finance rates are higher for this type of loan. Therefore, it is typically not a good option unless all other routes have been exhausted.

If your debt to income ratio is not optimal, a PACE loan might be the right choice to go solar. PACE financing still pencils out for many homeowners with sky high utility bills.

One main benefit of financing through PACE is that, should the home be sold, the balance of the solar loan transfers to the new homeowner. It is a relatively simple process for both the seller and buyer.

According to the

Department of Energy, there are PACE programs in California, Florida, and Missouri.

The Bottom Line

Going solar is a major investment with a significant long-term return. If you can't pay cash for solar, there are solar loans to help you start saving.

Solar loans are flexible because they typically require $0 down and offer loan terms between 8-20 years. This allows you to design a loan with a monthly payment that you are comfortable, and essentially choose your own electricity rate.

Team up with an Energy Advisor to get multiple solar quotes and find the right solar loan for you.

Solar loans frequently asked questions

How long does it take to pay off solar panels?

Solar loan terms typically range between 8-20 years. However, most loans allow for penalty-free pre-payments, which means you can pay off the loan at any time without paying an additional fee.

If you choose to pay cash for solar panels, the payback period is typically between 6-10 years, depending on your utility electricity price, energy consumption, and sun exposure.

Does a solar loan affect debt-to-income ratio?

Yes, taking out a solar loan typically increases your debt to income ratio, as it contributes toward your monthly debt payments.

For example, if you had $500 in debt payments and $1,500 in income before going solar, your DTI would be 33%. If you add $150 solar loan payment, your DTI would increase to 43% ($650/$1500).

What does reamortize mean?

To reamortize or recast a loan means to make a lump sum payment toward the principal loan balance in order to lower the monthly payments, as shown in the table below.

|

|

| Original monthly payment |

$127 |

| Reamortization lump payment |

$6,000 |

| New monthly payment |

$86 |

This is different from refinancing a loan for two reason:

- A refinance is an entirely new loan to replace the old loan, whereas a reamortization is a recalculation of the existing loan

- A reamortization requires a lump payment toward the loan balance while a refinance does not