See how much solar panels cost in your area

![]()

![]()

Solar Financing

Choosing how to finance your home solar system is a very exciting moment in the solar process. I mean, how often do you get to set your own price for electricity and choose when your solar savings kick in?

The way you choose to finance a solar system has a direct impact on the return on investment you see from your system. So, in this article, we’ll explore the three main solar financing options, and how each one affects your energy cost savings.

Jump ahead:

Let’s dive in with a quick review of the available solar financing options.

*

*

Solar financing options

Solar financing options are divided into two camps.

- Direct Ownership (you own the system)

- Third-Party Ownership (someone else owns the system)

Direct ownership of a solar system can be financed with a cash purchase or a solar loan. With the cost of solar panels plummeting and a 30% federal tax credit available, ownership has become the preferred option for homeowners in the last decade.

However, that’s likely to change beginning in late 2025.

The “One Big Beautiful Bill” signed into law, the federal solar tax credit claimed by homeowners (known as 25D) ends on December 31, 2025. Systems need to be installed by then for homeowners to claim this credit before it’s gone.

On the other hand, the 30% tax credit for Third-Party Owned residential solar (known as 48E) remains in effect through the end of 2027. This credit is claimed by the leasing company, and the savings are passed on to homeowners through lower rates.

Third-party ownership can be financed through a solar lease or power purchase agreement (PPA). Without a tax credit for homeowners to claim, leases and PPAs will offer greater savings for many homeowners.

| Cash purchase | Loan | Lease/PPA | |

| You own the system | X | X | |

| Greatest lifetime savings* | If installed before Dec. 31, 2025 | If installed before Dec. 31, 2025 | If installed after Dec. 31, 2025 |

| Immediate savings | X | X |

*Lifetime savings vary based on utility rate, state & local incentives, and other factors.

Now that we have an understanding of the options, let’s take a closer look at each one.

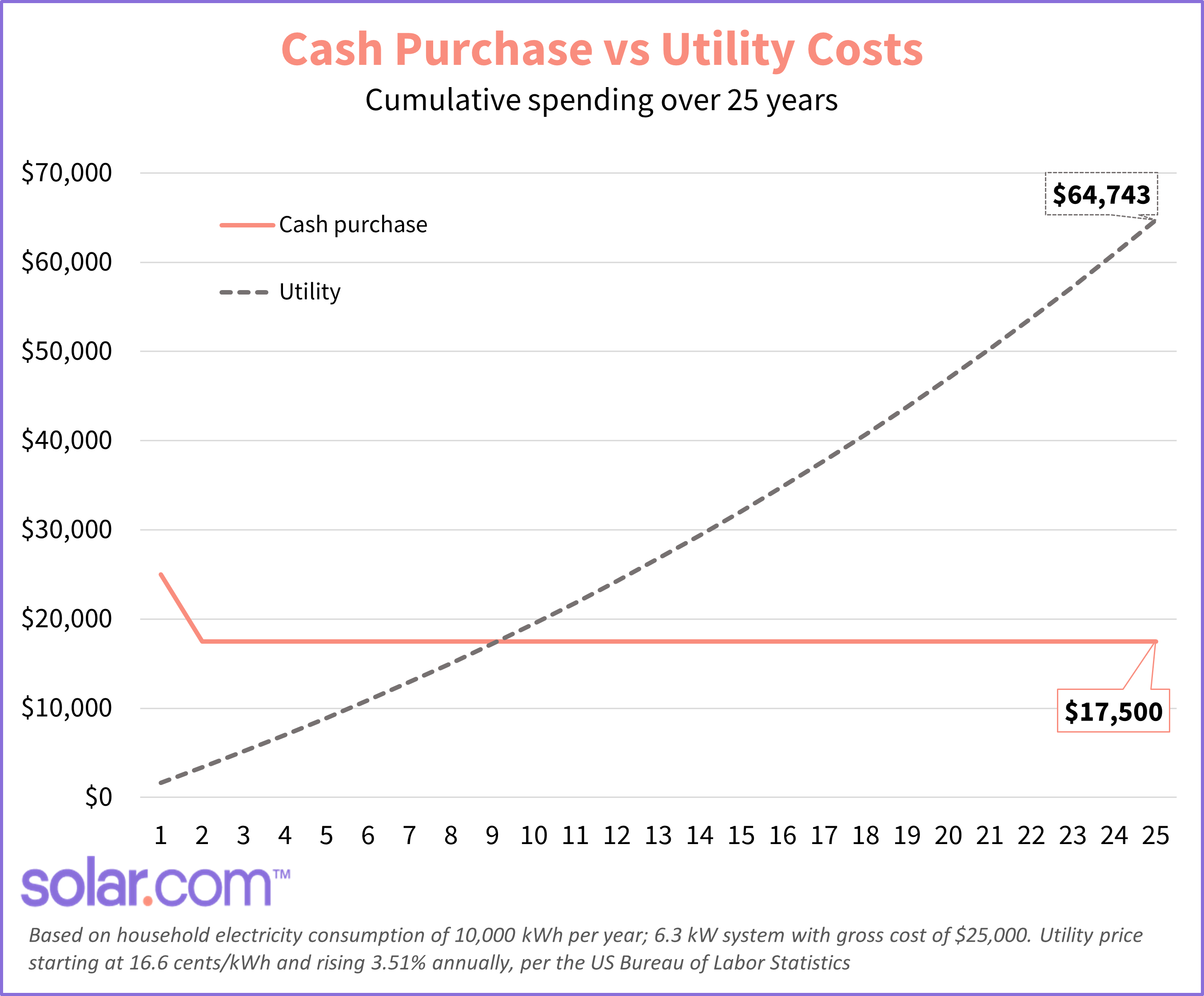

Buying solar panels with cash

In terms of accruing the greatest lifetime savings, cash is king.

If you have enough saved up, buying solar panels outright with cash payments will provide the greatest savings, for the simple fact that you avoid interest payments that come with solar loans.

One way to look at financing a solar system with cash is that you’re paying for 25 years of electricity in bulk. And if we’ve learned anything from Costco, everything is cheaper in bulk.

Get multiple solar quotes to see your savings potential.

How buying solar with cash works

Buying a solar power system with cash is relatively straightforward as there are no third-party solar financiers to deal with.

At Solar.com, there are 4 progress payments for a cash purchase:

- Down Payment/Deposit – $1,000 is typically due by the time your site visit is completed

- Due Upon Approval of Site Designs – $2,000 is due when you approve your ‘final site designs’ from the installer

- Due Upon Delivery of Materials – 60% of the remaining balance is due either when the equipment is delivered to you or on the first day of installation

- Due Upon Final Building Inspection – the rest of the remaining balance is due once your project passes city building inspection.

One thing to consider with a cash purchase is your payback period. Although you’ll enjoy the greatest lifetime savings, it takes time — typically 6-10 years — to recoup your initial investment.

If you’d rather spread out your payments and front-load your solar savings, it’s worth considering a solar loan to finance your system.

Related reading: 6 Reasons You Should Buy Solar Panels

Financing with a solar loan

If you do not have the cash up front to pay for your system, you can take out a solar loan. Solar loans are flexible and designed to accommodate the solar tax credit.

There is typically no down payment required for a solar loan and loan terms range from 8-25 years. So, by choosing a combination of down payment and loan term, solar borrowers are essentially able to dictate when and how they’re savings kick in.

As a rule of thumb:

- Shorter loan terms mean

- Higher monthly payments

- More lifetime savings

- Less money spent on interest

- Longer loan terms mean

- Lower monthly payments

- Less lifetime savings

- More money spent on interest

Here’s an example based on a $20,000 system for a homeowner with an average utility bill of $138 per month before going solar.

| TERM | 8-YEAR | 12-YEAR | 15-YEAR | 20-YEAR |

| Initial monthly payment | $183 | $129 | $133 | $125 |

| Lifetime interest paid | $3,662 | $4,645 | $10,082 | $16,230 |

| Lifetime savings | $43,260 | $42,252 | $36,888 | $30,828 |

As you can see, the 8-year loan provides the greatest overall savings, but the 20-year option provides the greatest immediate bill savings. Around 60% of solar borrowers go with a 12-year loan because it provides a balance of immediate bill reduction and long-term savings.

*

*

Solar loan rates and qualifications

Your loan payments and energy cost savings are also affected by interest rates and lending fees.

Interest rates are largely determined by market forces and Federal Reserve policy, but you can qualify for a lower rate based on your FICO credit score.

Generally, you need a 650 or higher FICO credit score to qualify for a solar loan. However, lenders usually offer lower interest rates for borrowers with credit scores between 680-719, and the best rates for borrowers with scores 720 and above

Although loan qualifications vary by lender, you typically need:

- A FICO credit score of 650 or higher

- A debt to income ratio (DTI) below 50%

- The name of the primary borrower needs to be on the title of the home getting the solar system.

In some cases, adding a co-borrower with a solid credit score and DTI can strengthen your application and increase your chances of getting loan approval.

Combo vs reamortizing solar loans

The other thing to consider is what kind of solar loan with which to finance your system. There are two types of solar-specific loans to know about: Combo and reamortizing loans.

Combo solar loans

As the name suggests, a combo loan is actually two loans. There’s a primary loan for the net cost of the solar system after the 30% federal tax credit is applied, and a bridge loan for the value of the tax credit.

So, if the contract price of your solar system is $25,000, then the primary loan balance would be $17,500 and the bridge loan balance would be $7,500.

Borrowers typically have 12-18 months to claim their solar tax credit and use it to pay off the bridge loan (although the funds can come from anywhere). If the bridge loan isn’t paid off in time, it’s rolled into the primary loan, which raises the monthly payments.

Here’s how that looks for a $25,000 system in a 20-year combo loan

| Borrower A | Borrower B | |

| Payment for months 1-18 | $110 | $110 |

| Month 18 | Bridge loan paid off | Bridge loan not paid off |

| Payment for months 19-240 | $110 | $160 |

The advantage of a combo solar loan is that your initial monthly payments are based on the lower net cost of the system. In other words, the solar tax credit is built into the loan before you even claim it.

Combo loans are the preferred choice for borrowers who are confident they have the tax liability to claim the solar tax credit in one year. However, if you are retired, or unsure you have enough tax liability for any reason, it’s worth considering a reamortizing solar loan.

Consult a licensed tax professional with questions regarding your tax liability.

Reamortizing solar loans

The second common type of solar loan is a reamortizing loan.

Reamortize is a bit of a mouthful, but it refers to making a lump sum payment on your loan in order to reduce your monthly payments. Like, for example, if you were expecting a tax credit worth 30% of the cost of your solar system…

Since most solar loan borrowers can expect to claim this tax credit, a reamortizing loan allows them to make a free, one-time lump sum payment to restructure their loan. Elsewhere in the lending world, there are servicing fees associated with reamortizing a loan.

Unlike a combo loan, the initial loan balance is based on the contract price of the system (ie what you paid for it). Let’s see how that looks for a $25,000 system in a 20-year reamortizing loan.

| Borrower A | Borrower B | |

| Payment for months 1-18 | $158 | $158 |

| Reamortization payment | $7,500 | $0 |

| Payments for months 19-240 | $108 | $158 |

The advantage of a reamortizing loan is that your monthly payments won’t go up if you are unable to claim the tax credit and apply it to your loan balance.

Related reading: Solar Loans: Good Debt or Bad Debt?

Property Assessed Clean Energy

One alternative solar loan option is the Property Assessed Clean Energy (PACE) program through the US Department of Energy.

Residential PACE pgrams are offered in California, Florida, and Missouri, and can be used to finance solar systems. In a PACE loan, the “debt is tied to the property as opposed to the property owner(s).”

From our blog: All You Need To Know About Solar Home PACE Financing

Solar financing options for third-party ownership

Now that we’ve covered the financing options for owning solar panels, let’s explore how to go solar without actually owning the system.

There are two ways to finance a solar system that someone else ones:

- Solar leases

- Power purchase agreements (PPAs)

Let’s start with the solar lease.

Solar Leases

A solar lease is similar to a solar loan in the sense that both are forms of going solar with no upfront payment. But the similarity pretty much stops there.

With a solar lease, you are renting your system from a third-party owner. You pay the owner a fixed monthly payment for the full term of the lease, which is typically 15-20 years, instead of paying your utility company for electricity.

Solar leases may include an escalator, which raises your monthly payment by 2-5% every year. So, if you had a 20-year lease with an initial payment of $125 per month and a 3.5% escalator, your monthly payment would eventually reach $240 by year 20.

| Year | Monthly payment |

| 1 | $125 |

| 5 | $143 |

| 10 | $170 |

| 15 | $202 |

| 20 | $240 |

Leases typically offer immediate bill savings, and the leasing company is responsible for monitoring and maintaining the system.

Other noteworthy parts of third-party ownership include:

- The installer collects the 30% tax credit, not you

- The system adds limited value to your home

- Leased solar systems can slow and complicate home sales since transferring them involves a third party

Leases will become more prevalent beginning in late 2025 as homeowners lose direct access to the 30% federal solar tax credit. In an era of fast-rising utility rates, they offer a simple way to lower and flatten your essential energy costs.

Solar Power Purchase Agreements (PPAs)

Power Purchase Agreements are very similar to solar leases. The major difference is that instead of a flat monthly rate, you pay a monthly fee based on how much the system produces.

The idea is that this rate is lower than what you pay a utility for electricity. Similar to leases, PPAs may include escalators, and it’s important to thoroughly read any Third-Party Ownership contract to understand the terms of your arrangement.

Like a solar lease, you do not own the system in a PPA.

Should I buy or lease a solar system?

In 2025, deciding between ownership or a lease is a simple question of whether you can get installed in time to claim and monetize the 30% solar tax credit.

If you can, owning your solar system and claiming the tax credit often provides the greatest lifetime savings potential, and the benefits of added property value.

If a 2025 installation isn’t possible, leasing provides a great alternative to ownership. You can lock in a low, predictable cost for electricity instead of paying more and more each year to your utility.

The bottom line

While you may hear of the “high upfront cost” of going solar, financing a solar system is flexible and can be designed to meet your energy cost savings goals.

While buying a system with cash presents the greatest opportunity for return on investment, you can also use a solar loan to spread your payments over time and start saving money sooner.

Connect with an Energy Advisor to discuss your solar financing options today.

Solar financing FAQs

Can you finance solar panels?

Yes, there are two types of loans specifically designed to finance solar panels: combo loans and reamortizing loans. In most cases, in order to qualify for a solar loan you need a minimum FICO credit score of 650, a debt-to-income ratio lower than 50%, and a primary borrower’s name needs to on the title of the home.

How does solar financing work?

There are two types of solar loans: combo and reamortizing. In a combo loan, there is a primary loan for the net cost of the system and a bridge loan for the value of the 30% federal solar tax credit. This essentially allows solar borrowers to use the tax credit as a delayed downpayment on their loan.

In a reamortizing loan, the loan balance is the contract price of the system. This loan allows for a free, one-time lump sum payment to reduce monthly payments. Borrowers typically reamortize within 12-18 months, after they have received their solar tax credit.

Is financing solar panels worth it?

There are several benefits to financing a solar system. First, it allows homeowners to go solar — and start accumulating energy cost savings — even if they don’t have enough cash to purchase a system outright.

Second, financing solar panels allows you to front-load your energy cost savings with a zero-down loan. Typically, the payments on a solar loan are lower than the average monthly utility payment.

Related Articles

See how much solar panels cost in your area.

Please enter a valid zip code.

Zero Upfront Cost. Best Price Guaranteed.