Is It Better to Lease Or Buy Solar Panels?

Home solar is a means to long-term energy savings for a vast majority of US homeowners, but exactly how much you save depends on whether you lease or buy solar panels.

We’ll be the first to admit that solar financing isn’t exactly the sexiest topic in the world and it can feel a bit overwhelming at first. However, the way you finance your solar panels can make the difference of tens of thousands in energy savings over the life of the system.

So we’ve created this guide to help you explore the basics of leasing vs buying solar panels. In this article, we’ll cover:

- Leasing vs buying solar panels

- Ways to buy solar panels

- Ways to lease solar panels

- Is it better to buy or lease solar panels?

- Frequently asked questions

Let’s dive in with the difference between buying and leasing solar panels.

Lease or buy solar panels: What’s the difference?

There are three major differences between buying and leasing solar panels:

- Who owns the system

- Who collects the solar incentives

- What happens when you sell your home

If you purchase a solar system, either with cash or a loan, you own the system and receive 100% of the benefits that come with it. That includes the 30% federal solar tax credit (if the system is installed before the end of 2025!) and any other state, local, or installer incentives.

When you sell your home, the solar system is treated as an attached appliance like a furnace or air conditioner — it’s sold as part of the home. In fact, multiple studies have shown that homes with solar systems sell faster and for more money.

If you lease a solar system, the company you lease from owns the system. You are essentially renting the system from a solar company, similar to leasing a car or renting an apartment. That means you aren’t responsible for monitoring, maintaining, and repairing the system in the rare instance of a component failure. However, you also don’t directly benefit from any of the incentives. The company that owns the system claims tax credits and rebates, and then factors the savings into lower payments for you.

Leases are also more difficult to transfer in a home sale, and do not add home value like owned systems do.

| Cash Purchase | Purchase w/ Loan | Lease | |

| No Cash Out of Pocket | X | X | |

| Receive Tax Credit | X | X | |

| First Year Savings | X | X | |

| Greatest Lifetime Savings* | If installed before Dec. 31, 2025 | If installed before Dec. 31, 2025 | If installed after Dec. 31, 2025 |

| Own Your Equipment | X | X | |

| Added Home Value | X | X |

*With the tax credit for homeowner-owned systems ending on December 31, 2025, lifetime savings potential will vary based on your utility rate and locally available incentives.

Let’s take a quick look at how each financing method works.

Two ways to buy solar panels

Much like a house or car, home solar systems can be purchased with cash or a loan. Here are the basics of buying a solar panel system.

Buying with cash

Paying cash is the simplest way to buy a solar system and presents the greatest opportunity for energy savings. That’s because you are avoiding the interest payments on a loan and the escalating payments on a lease. And, some installers offer a discount for paying in cash, which increases your overall savings.

Buying a solar system with cash typically consists of four payments. The exact benchmarks and payment amounts will vary from installer to installer.

Here’s what a cash payment schedule may look like:

- Down payment or deposit – $1,000 due upon completion of site visit

- Design approval – $2,000 due upon approval of your final system design

- Materials deposit – 60% of the remaining balance is used to purchase materials for your installation

- Building inspection – The remaining balance is due after the installed solar system passes city building inspection

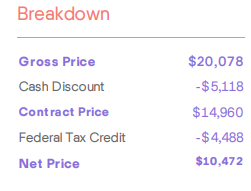

It’s important to note that the 30% federal solar tax credit kicks in after you’ve paid for the system (and this will not be available for systems installed after December 31, 2025!). That means you pay the full contract price in cash and end up with the lower net cost after you claim your tax credit.

Buying with solar loans

Many homeowners use loans to purchase solar panels because they require less cash upfront and still provide substantial long-term energy savings.

Solar loans typically have the following qualifications:

- The borrower is the owner of the home getting solar panels

- The home getting solar is a primary residence

- A minimum credit score of 650

- A debt-to-income (DTI) ratio that does not exceed 50%

With zero-down payment options and loan terms as long as 20 years, and follow a “reamortizing” loan structure.

Re-amortizing loans

Re-amortizing loans work similarly to a home loan with a free one-time refinance. This loan structure is commonly used by homeowners that don’t expect to have the tax liability to quickly collect the 30% solar tax credit. Consult a licensed tax professional with questions regarding your tax liability.

In a re-amortizing loan, the loan balance is based on the contract price of the system. This makes for higher payments upfront than a combo loan. However, as the name suggests, borrowers can re-amortize by making a lump sum payment to lower the monthly loan payments.

One way to think of it is delaying a down payment until you receive your solar tax credit. However, the re-amortization payment can come from anywhere – inheritance, holiday bonus, selling baseball cards on eBay.

Here’s an example of a 20-year re-amortizing loan with a contract price of $25,000 and a re-amortization with the value of the 30% tax credit after year two.

| Age of loan | Monthly payment |

| 1-24 months | $135 |

| Re-amortization | $7,500 lump payment |

| 25-240 months | $93 |

It’s important to note that the lender has nothing to do with claiming the solar tax credit. That’s between you, the IRS, and a licensed tax professional.

Two ways to lease solar panels

Solar panels can also be leased, similar to renting an apartment or leasing a car. There are two basic types of solar lease agreements: Fixed monthly leases and Power Purchase Agreements (PPAs).

Fixed monthly solar lease

Fixed monthly solar leases are pretty straightforward. The solar company installs a system on your roof, and instead of paying your utility bill, you make a lower monthly lease payment on the solar system.

For example, if your utility bill is $140 a month, your monthly solar lease payments might be $99 for the first year. That saves you $41 a month and $492 in the first year.

Solar leases usually last 20 or 25 years and may include an annual escalator. The escalator raises the monthly payment over time, typically by around 3% per year. So if the payments are $99 a month in the first year, they would be ~$102 per month in the second year, ~$105 in the third year, and so on.

Escalators increase your payments over time, but typically at a lower pace than your utility rate rises.

| Lease Year | Monthly Lease Payment | Annual Cost |

| 1 | $99 | $1,188 |

| 5 | $111.43 | $1,337.10 |

| 10 | $129.17 | $1,550.07 |

| 15 | $149.75 | $1,796.96 |

| 20 | $173.60 | $2,083.17 |

20-year solar lease with a 3% annual escalator.

Solar leases offer immediate energy cost savings without the responsibilities of owning and maintaining a solar system.

Power purchase agreement (PPA)

In a PPA, the homeowner pays for the power generated from the solar system instead of a flat monthly rate for the equipment.

The idea is to pay a lower rate for solar electricity than for grid electricity. So, a PPA provider may offer you a rate of 12 cents per kilowatt hour, whereas your utility charges 16.6 cents per kilowatt hour.

Like a solar lease, PPAs may include escalators that increase the price each year, although typically at a lower rate than your utility rate rises.

Is it better to buy or lease solar panels?

In the last decade, solar ownership offered greater lifetime savings potential. However, with the 30% tax credit homeowner-owned systems ending on December 31, 2025, we’re likely to see a shift back to leases and PPAs. The tax credit for third-party owned systems remains in effect through 2027, and many homeowners will see greater savings potential from leasing than ownership.

FAQs

Is it better to buy or lease solar panels?

With direct access to a 30% tax credit, solar ownership (cash or loan purchase) typically offers greater savings benefits than leasing. However, with the homeowner-claimed tax credit ending at the end of 2025, many households will see greater savings potential in a lease or PPA.

What is the downside of leasing solar panels?

There are a few downsides to leasing solar panels. First, the energy savings potential is lower than buying solar panels and claiming a 30% tax credit. (However, without a 30% tax credit for ownership, we’ll likely see this leases and PPAs provide greater savings potential for most households). Also, solar leases can be difficult to transfer during a home sale, whereas owned panels typically increase home value.

Is it better to finance or pay cash for solar panels?

In terms of long-term savings, paying cash for solar panels provides a greater potential return on investment. However, solar loans are quite common, and there is still plenty of energy savings to be had for homeowners who finance their solar system.