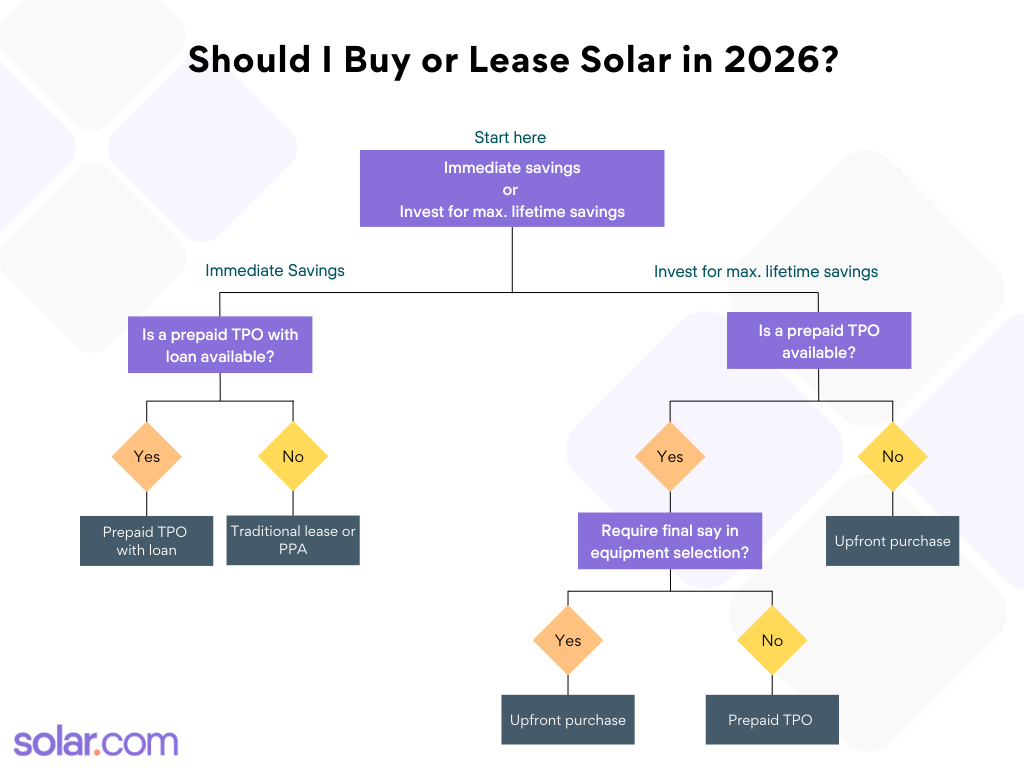

What is an HDM Prepaid Solar PPA? An HDM Prepaid Solar Power Purchase Agreement (PPA) is a solar financing model that allows California homeowners to prepay for 20-25 years of solar energy in a single upfront payment at a significant discount over direct ownership. By leveraging the business-claimed federal solar tax credit and commercial depreciation, HDM provides the long-term savings of solar ownership with the maintenance-free benefits of a lease—making it one of the most effective ways to combat rising utility rates under NEM 3.0.

HDM Prepaid PPA: Key Benefits at a Glance

The HDM (Homeowner Debt Monetization) model is designed to bridge the gap between traditional leasing and full ownership. Here is why it is becoming the preferred choice for California homeowners in 2026:

- Massive Upfront Savings: Because the provider claims the 48E federal solar tax credit and accelerated depreciation, they pass those savings to you as a deep discount on the system price—effectively lowering your entry cost by 20-30%.

- $0 Monthly Solar Bills: Unlike a standard PPA or lease, there are no monthly installments or “escalators.” Once you prepay, your solar energy is covered for the life of the agreement, protecting you from utility rate hikes.

- Guaranteed Performance: The system is professionally monitored and maintained by the provider. If the panels don’t produce the energy promised, you are often compensated for the shortfall, removing the risk of ownership.

- A Clear Path to Ownership: Most HDM contracts include a $0 or nominal fee buyout option (typically after year 6). You get the tax-advantaged pricing now and full asset ownership later.

- NEM 3.0 Optimization: By pairing a prepaid PPA with battery storage, you can maximize your “self-consumption” and avoid the low export rates mandated by California’s newest utility rules.

Jump ahead:

- Why California Homeowners Are Looking Beyond Traditional Solar Leases and PPAs

- How Does an HDM Prepaid PPA Work?

- Who Should Consider the HDM Prepaid PPA?

- Common Questions and Risks to Watch Out For

HDM Renewable Finance is not affiliated with solar.com. Information is provided for educational purposes only and is not tax advice or an endorsement of the HDM product. HDM Renewable Finance trademark, names, and copyrights are the property of HDM Renewable Finance.

Why California Homeowners Are Looking Beyond Traditional Solar Leases and PPAs

California homeowners face the highest electricity rates in the country, with costs rising much faster than inflation. However, with the elimination of the consumer solar tax credit at the end of 2025 and with new utility rules, such as NEM 3.0, significantly reducing the value of solar export credits, the path to solar savings has become more complex.

Many families are now seeking solar financing options that provide immediate savings and long-term price certainty without large monthly payments.

Historically, solar leases and Power Purchase Agreements (PPAs) were the non-cash alternatives. But a new model is disrupting the market: Prepaid Solar PPAs and Leases, including ones offered by HDM Renewable Finance.

Here’s the key difference:

- Traditional leases & PPAs apply some or all of the 48E tax credit value as a reduction to monthly payments.

- HDM Prepaid PPA applies some or all of the 48E tax credit value as a reduction in the upfront cost of the system (which can be financed or paid for outright).

Let’s recap the basics of traditional leases and PPAs so we can compare these options to HDM’s Prepaid PPA.

What Is a Traditional Solar Lease?

A solar lease is one of the oldest and simplest financing models. Essentially, the homeowner “rents” the solar system for a fixed monthly fee over a period (usually 20-25 years).

The installation company (the lessor) owns and maintains the system. The homeowner benefits from the electricity produced but does not own the asset; they simply realize the savings generated from the solar on their roof. A solar lease is like a coupon for your utility bill.

| Pros of a Solar Lease | Cons of a Solar Lease |

| Little to no upfront cost | No access to the Federal Tax Credit (ITC) for the homeowner |

| Maintenance and repairs are included | You do not own the system (it’s a rental) |

| Predictable fixed monthly payments | Lease payments can raise costs over time through rate escalators, which may increase Day 1 savings, but minimize the long-term savings potential of the array. |

| Easy to transfer from utility bills | Can complicate or delay selling your home |

What Is a Standard Power Purchase Agreement (PPA)?

A standard PPA is similar to a lease, but instead of paying a fixed monthly rent, you pay for the electricity the system produces on a per-kilowatt-hour (kWh) basis.

The PPA provider owns and maintains the system. Your rate per kWh is almost always lower than your utility’s rate, but often includes an annual escalator (e.g., 2.9% increase per year). Most PPAs, however, provide a protection that guarantees the PPA rate will never exceed the avoided retail (utility) rate. This ensures savings for the homeowner.

How Does an HDM Prepaid PPA Work?

The HDM Prepaid Solar PPA model combines the core benefits of system ownership (long-term savings, no monthly bills) with the simplicity of a managed contract. HDM (Homeowner Debt Monetization) is a financial product that allows the homeowner to prepay the cost of their solar energy contract at a significantly discounted rate.

The HDM model is able to offer a lower upfront cost because the financing company claims and monetizes the 48E Clean Electricity Investment Tax Credit (ITC) and accelerated depreciation benefits. This is especially valuable in 2026, with the 25D tax credit no longer available for homeowners to claim directly.

HDM Prepaid PPA: Step by Step

- The homeowner is offered a prepayment amount, typically around 70% of the cost to purchase a comparable system.

- Homeowner makes a single upfront payment (or finances the balance through a low-interest personal loan or HELOC).

- The Prepaid PPA provider owns the system and claims applicable incentives.

- The homeowner enjoys $0 ongoing monthly payments for solar energy (or fixed loan payments, if financed).

- After a set period (often around 6 years), the homeowner has the option to buyout the financing agreement and take ownership of the system.

HDM Prepaid PPA vs. Lease & Standard PPA: Side-by-Side Comparison

| Factor | Traditional Lease | Standard PPA | HDM Prepaid PPA |

| Upfront Cost | Low ($0–$1,000) | Low ($0–$1,000) | High (but discounted by ITC benefits) |

| Monthly Solar Bills | Fixed payment ($100–$150) | Variable (e.g., $0.18/kWh) | **None ($0)** |

| Tax Credit (ITC) Access | No (Lease provider claims) | No (PPA provider claims) | Indirect (via upfront discount) |

| Maintenance | Included | Included | Included until ownership transferred to homeowner |

| Ownership | No | No | Transfer after ~6 years |

| Long-Term Savings | Moderate (payment escalators may apply) | Moderate (rate escalators may apply) | Highest Potential (no monthly bills) |

Why the Prepaid PPA is Ideal in California in 2026

California’s unique energy landscape makes the prepaid PPA especially attractive:

- Protection from Rate Hikes: With PG&E, SCE, and SDG&E rates being among the highest in the U.S., a prepaid PPA acts as a fixed-price hedge against future utility rate inflation.

- Predictable Savings under NEM 3.0: The new NEM 3.0 rules have cut the value of excess solar exported to the grid. A Prepaid PPA provides savings by eliminating the monthly electric bill component, relying less on the volatile export credit value.

- Monetizing the ITC: With the homeowner-claimed tax credit (25D) eliminated, the prepaid model allows homeowners to go solar at around 70% of the cost of purchasing a solar system without a tax credit.

Who Should Consider the HDM Prepaid PPA?

| Good Fit | Not Ideal For |

| Homeowners who want $0 monthly solar bills immediately. | Homeowners who may move within the next 5 years. |

| Those want want to pay upfront for solar at roughly 70% of the cost to purchase a system. | Homeowners who prefer sole ownership over their solar & battery system. |

| Households planning to stay in their home for 6+ years. | Households with very low energy usage, where the initial investment might not be justified. |

Common Questions and Risks to Watch Out For

Prepaid PPAs are powerful, but the contract details matter. Homeowners must understand the fine print.

Q: What is the true cost of ownership transfer with a Prepaid PPA?

A: The ownership transfer (often after 6 years) typically has a nominal, pre-determined fee. Crucially, once ownership transfers, the homeowner is then responsible for maintenance, repairs, and insurance, but they also gain the full asset value and may be eligible for state or local incentives that did not apply before.

Q: Is there a guaranteed minimum energy production?

A: Yes. Most reputable Prepaid PPAs include a legally binding Production Guarantee. This means if the system produces less than the contracted kWh due to factors like system malfunction, the PPA provider must compensate the homeowner for the difference. Always ask for the specific Performance Ratio and the compensation rate per kWh.

Q: How easy is it to sell a home with a Prepaid PPA?

A: Prepaid PPAs are generally easier to transfer than traditional solar leases. Because the energy is already paid for, the new homeowner inherits a system with $0 monthly payments, which is a highly attractive selling point. However, the current homeowner should always have the contract’s explicit transfer requirements and associated fees ready for the buyer.

Q: Can I add a solar battery with a Prepaid PPA?

A: As long as the value provided by the battery exceeds the cost of installing the battery, Prepaid PPAs, in almost every circumstance, allow battery integration from the start or offer easy add-on options. Given the changes under NEM 3.0 that favor solar-plus-storage, ensure your contract allows for battery integration to maximize your savings.

The Bottom Line

For many California homeowners, the HDM Prepaid Solar PPA offers a smarter path to solar savings than a traditional lease. With no monthly bills, included maintenance, and options for delayed ownership, it offers financial stability in a state where utility costs are anything but.

As with any contract, the details matter. Always ask for clear, written answers regarding production guarantees, ownership transfer, and buyout options before signing.

When available, get competing quotes from qualified local contractors and select the right technology for your project.